Wages are one of the major portion in the total cost of production. There is always a chance of fraud in wage payment. Therefore, an effective administrative and accounting control system must be implemented by the management to minimize fraud and to keep the labor cost minimum. As already stated, a number of departments are set up for the effective utilization of labor force and its proper accounting and controlling. These departments are required to work in a coordinated manner and to support the management in controlling labor cost by recording and reporting their activities on regular basis. The management should evaluate and revise its controlling system to find out leakages and to stop such leakages in time. Fraud in wage payment may result in various ways like inclusion of dummy worker in pay-roll, manipulating hours, recording extra overtime, using a wrong wage rate and registering absent workers.

Sunday, 30 May 2010

Following are the main differences between piece rate system and time rate system.

1. Meaning

Piece rate system is a method of wage payment to workers based on the quantity of output they have produced. Time rate system is a method of wage payment to workers based on time spent by them for the production of output.

2. Nature Of Payment

Piece rate system pays the workers according to the units of output produced. Time rate system pays the workers according to the time spent in the factory.

3. Emphasis

Piece rate system gives emphasis on larger quantity of output. Time rate system emphasis on better quality of output.

4. Discrimination

Piece rate system discriminates the workers and pays more wages to efficient and skilled workers. Time rate system does not discriminate the workers and pays the same wages to efficient and inefficient workers.

5. Supervision

Piece rate system requires strict supervision to get the required quality output. Time rate system requires strict supervision to get required quantity of output.

6. Determination Of Labor Cost

Piece rate system helps to fix per unit labor cost in advance. Time rate system does not help to fix labor cost per unit in advance.

7. Flow Of Production

Piece rate system does not bring uniformity in the flow of production and causes an excessive wastage of inputs. Time rate system helps maintain a uniform flow of production and ensures an efficient use of materials, tools and equipments.

1. Meaning

Piece rate system is a method of wage payment to workers based on the quantity of output they have produced. Time rate system is a method of wage payment to workers based on time spent by them for the production of output.

2. Nature Of Payment

Piece rate system pays the workers according to the units of output produced. Time rate system pays the workers according to the time spent in the factory.

3. Emphasis

Piece rate system gives emphasis on larger quantity of output. Time rate system emphasis on better quality of output.

4. Discrimination

Piece rate system discriminates the workers and pays more wages to efficient and skilled workers. Time rate system does not discriminate the workers and pays the same wages to efficient and inefficient workers.

5. Supervision

Piece rate system requires strict supervision to get the required quality output. Time rate system requires strict supervision to get required quantity of output.

6. Determination Of Labor Cost

Piece rate system helps to fix per unit labor cost in advance. Time rate system does not help to fix labor cost per unit in advance.

7. Flow Of Production

Piece rate system does not bring uniformity in the flow of production and causes an excessive wastage of inputs. Time rate system helps maintain a uniform flow of production and ensures an efficient use of materials, tools and equipments.

Saturday, 29 May 2010

The time rate system is that system of wage payment in which the workers are paid on the basis of time spent by them in the factory. Under this system, the workers and employees are paid wages on the basis of the time they have worked rather than the volume of output they have produced. Hence, according to this system, wages are paid on hourly, weekly or monthly basis. Under time rate system, the wages earned by a worker is determined by using the following formula.

Wages Earned = Time spent(Attended) x Wage rate per hour/day/week/month

Advantages Of Time Rate System

The following are some of the important advantages of time rate system of wage payment:

* Time rate system is simple to understand and easy to calculate.

* Time rate system is quite useful for organizations that use costly inputs for quality outputs.

* Time rate system is beneficial for average and below workers.

* Time rate system assures regular income and creates the feeling of economic security among the workers.

* Time rate system does not discriminate the workers and is preferred by trade unions.

Disadvantages Of Time Rate System

The following are some notable disadvantages of time rate system of wage payment.

* Time rate system does not help in increasing output and improving efficiency as there is no correlation between effort and reward.

* Time rate system is not justifiable between efficient and inefficient workers and skilled and unskilled workers.

* Time rate system pays for idle time, which increases the cost of production.

Time rate system encourages a g0-slow tendency among workers during working hours and encourages them to work overtime.

* It is difficult to estimate exact labor cost in advance.

* It requires strict supervision to get the required quantity of output.

Wages Earned = Time spent(Attended) x Wage rate per hour/day/week/month

Advantages Of Time Rate System

The following are some of the important advantages of time rate system of wage payment:

* Time rate system is simple to understand and easy to calculate.

* Time rate system is quite useful for organizations that use costly inputs for quality outputs.

* Time rate system is beneficial for average and below workers.

* Time rate system assures regular income and creates the feeling of economic security among the workers.

* Time rate system does not discriminate the workers and is preferred by trade unions.

Disadvantages Of Time Rate System

The following are some notable disadvantages of time rate system of wage payment.

* Time rate system does not help in increasing output and improving efficiency as there is no correlation between effort and reward.

* Time rate system is not justifiable between efficient and inefficient workers and skilled and unskilled workers.

* Time rate system pays for idle time, which increases the cost of production.

Time rate system encourages a g0-slow tendency among workers during working hours and encourages them to work overtime.

* It is difficult to estimate exact labor cost in advance.

* It requires strict supervision to get the required quantity of output.

The piece rate system is that system of wage payment in which the workers are paid on the basis of the units of output produced. Piece rate system does not consider the time spent by the workers. Piece rate system is the method of remunerating the workers according to the number of unit produced or job completed. It is also known as payment by result or output. Piece rate system pays wages at a fixed piece rate for each unit of output produced. The total wages earned by a worker is calculated by using the following formula.

Total Wages Earned= Total units of outputs produced x Wage rate per unit of output.

Total Wages Earned= Output x Piece Rate

Advantages Of Piece Rate System

The following are some important advantages of piece rate system of wage payment.

* Piece rate system pays wages according to the output produced by the workers. It encourages efficient workers.

* Piece rate system helps to reduce idle time.

* Piece rate system gives incentives to the workers to adopt a better method of production for increasing their production and earning.

* Piece rate system helps the management to determine the exact labor cost per unit for submitting quotation.

* Piece rate system reduces per unit cost of production due to increased volume of production.

* Piece rate system requires less supervision cost.

Disadvantages Of Piece Rate System

The following are the notable disadvantages of piece rate system

* Piece rate system does not help in producing quality output as the workers are concentrated more on quantity instead of quality.

* Piece rate system does not help for a uniform flow of production and makes difficult to regulate the production schedule.

* It is very difficult to fix an acceptable and reasonable piece rate for each item of output or job.

* Piece rate system adversely affect the workers' health as well.

* It requires extra supervision cost for quality output and effective use of materials, tools and equipment.

The system of wage payment is the method adopted by manufacturing concerns to remunerate workers. It is the way of giving financial compensation to the workers for the time and effort invested by them in converting materials into finished products. It indicates the basis of making payment to the workers, which may be either on time basis or output basis. The selection of the system depends on the type and nature of the concern and its products. The wage payment systems can be divided into two main systems as follows.

1. Piece rate system

2. Time rate system

Importance Of Wage Payment System

The amount of wages paid to the workers is one of the major elements of cost. It has a great bearing on the cost of production and profitability of the concern. Hence, every concern is required to adopt a fair system of wage payment.

The importance of wage payment system can be summarized as follows:

* Wage payment system facilitates the preparation of wage plan for future.

* Wage payment system helps to determine the cost of production and the profitability of the organization.

* Wage payment system determines the amount of earning of the workers and their living standards.

* Wage payment system affects the interest and attitude of the workers.

* Wage payment system determines the level of satisfaction of the workers and affects the rate of labor turnover.

* Wage payment system helps in recruiting skilled, experienced and trained workers.

* Wage payment system helps to increase the productivity and goodwill of the organization.

Essential Characteristics Of A Good Wage Payment System

A sound system of wage payment is one that satisfies employer and employee by fulfilling following criteria.

* Wage payment system should be fair and justifiable to the workers and organization.

* Wage payment system should help in maximizing workers' satisfaction and minimizing labor turnover.

* Wage payment system should assure minimum guaranteed wages to all workers.

* Wage payment system should assure equal pay for equal work.

* Wage payment system should provide more wages to efficient and skilled workers.

* Wage payment system should follow government policy and trade union's norms.

* Wage payment system should be simple and understandable to all the workers.

* Wage payment system should help in improving performance and productivity of the workers.

* Wage payment system should be flexible enough to suit the needs of the organization.

1. Piece rate system

2. Time rate system

Importance Of Wage Payment System

The amount of wages paid to the workers is one of the major elements of cost. It has a great bearing on the cost of production and profitability of the concern. Hence, every concern is required to adopt a fair system of wage payment.

The importance of wage payment system can be summarized as follows:

* Wage payment system facilitates the preparation of wage plan for future.

* Wage payment system helps to determine the cost of production and the profitability of the organization.

* Wage payment system determines the amount of earning of the workers and their living standards.

* Wage payment system affects the interest and attitude of the workers.

* Wage payment system determines the level of satisfaction of the workers and affects the rate of labor turnover.

* Wage payment system helps in recruiting skilled, experienced and trained workers.

* Wage payment system helps to increase the productivity and goodwill of the organization.

Essential Characteristics Of A Good Wage Payment System

A sound system of wage payment is one that satisfies employer and employee by fulfilling following criteria.

* Wage payment system should be fair and justifiable to the workers and organization.

* Wage payment system should help in maximizing workers' satisfaction and minimizing labor turnover.

* Wage payment system should assure minimum guaranteed wages to all workers.

* Wage payment system should assure equal pay for equal work.

* Wage payment system should provide more wages to efficient and skilled workers.

* Wage payment system should follow government policy and trade union's norms.

* Wage payment system should be simple and understandable to all the workers.

* Wage payment system should help in improving performance and productivity of the workers.

* Wage payment system should be flexible enough to suit the needs of the organization.

The need of labor cost control arises to fulfill the following purposes.

* Labor cost control is important to make economic utilization of labor force in production process.

*Labor cost control is important to obtain maximum quantity of output with the least amount of materials and other resources.

* Labor cost control helps to obtain better quality output with the least effort and time of workers.

* Labor cost control reduces the cost of production of products manufactured or services rendered.

* Labor cost control ensures the satisfaction of the workers by creating a good working environment in the factory.

* Labor cost control helps to adopt the fair system of wage payment and to minimize labor turnover.

* Labor cost control is helpful in minimizing wastage of materials by workers , idle time and unusual overtime work.

* Labor cost control is helpful to maintain safety working environment.

* Labor cost control is important to keep complete records of the employees and to supply information to the management regarding availability, efficiency, utilization and absenteeism of the workers.

* Labor cost control is very useful to increase the profitability and competitiveness of the organization.

Labor cost covers one of the major portion of the total cost of a product or job. It may increase unnecessarily due to inefficiency of workers, wastage of materials by workers, idle time, unusual overtime work and high labor turnover. Hence, the management should devise effective techniques for controlling labor cost to ensure maximum outputs of better quality at low cost through proper utilization of the labor force.

Basically, management is concerned with controlling labor cost. Labor cost control involves such systems, procedures, techniques and tools used by the management in order to keep the labor cost of the product or job as minimum as possible. Labor cost control consists of a number of such regular activities which are carried on by various departments of the organization in a coordinated manner to ensure the availability of the best employees and their optimum utilization. It is the system followed by the management to maximize quality output at a minimum cost. Labor cost control includes the process of developing various forms, studying and recording the activities and performance of workers, calculating the correct amount of wages and making payment in time. It also include the process of analyzing and reporting labor cost to the management for planning and decision making.

Basically, management is concerned with controlling labor cost. Labor cost control involves such systems, procedures, techniques and tools used by the management in order to keep the labor cost of the product or job as minimum as possible. Labor cost control consists of a number of such regular activities which are carried on by various departments of the organization in a coordinated manner to ensure the availability of the best employees and their optimum utilization. It is the system followed by the management to maximize quality output at a minimum cost. Labor cost control includes the process of developing various forms, studying and recording the activities and performance of workers, calculating the correct amount of wages and making payment in time. It also include the process of analyzing and reporting labor cost to the management for planning and decision making.

Thursday, 27 May 2010

Proper study, analysis and control of labor costs are important to all manufacturing concern because of the following reasons.

* Labor cost is main element of cost which covers one of the major portions of the total cost of a product or job.

* Labor cost is more difficult to control as compared to material cost due to the involvement of human element.

* Labor cost is affected due to a change in government policy and requirement of trade union.

* Labor cost is adversely affected due to dissatisfaction , irregularity, inefficiency, idle time, high labor turnover, lack of interest and negative attitude of the workers.

* Labor cost is important from the fact that the direct labor cost is taken as the basis of estimating the amount of factory overheads while determining the product cost.

* Labor cost is main element of cost which covers one of the major portions of the total cost of a product or job.

* Labor cost is more difficult to control as compared to material cost due to the involvement of human element.

* Labor cost is affected due to a change in government policy and requirement of trade union.

* Labor cost is adversely affected due to dissatisfaction , irregularity, inefficiency, idle time, high labor turnover, lack of interest and negative attitude of the workers.

* Labor cost is important from the fact that the direct labor cost is taken as the basis of estimating the amount of factory overheads while determining the product cost.

Wednesday, 26 May 2010

Like the labor, labor costs are of two types such as follows

1. Direct Labor Cost

Direct labor cost is the amount spent by the factory for those workers involved directly in the manufacturing process. It can be measured conveniently and accurately on per unit of output basis. Direct labor cost can be identified and allocated to the specific job or process or product. It forms a part of the prime cost. The examples of direct labor costs are the payments made to the workers engaged in making table, printing a book and constructing a dam etc.

2. Indirect Labor Cost

Indirect labor cost is the amount spent by the factory for those workers who are not directly engaged in the production process. Indirect labor cost refers to the expenses incurred in remunerating such workers who assist the direct labor to complete the manufacturing processes. It can not be identified and measured accurately on per unit of output basis. It is incurred for the benefits of a number of cost centers. It forms a part of the overhead costs. Payment made to the sweepers, watchmen, cleaners, supervisors and accounting personnel are the examples of indirect labor cost.

1. Direct Labor Cost

Direct labor cost is the amount spent by the factory for those workers involved directly in the manufacturing process. It can be measured conveniently and accurately on per unit of output basis. Direct labor cost can be identified and allocated to the specific job or process or product. It forms a part of the prime cost. The examples of direct labor costs are the payments made to the workers engaged in making table, printing a book and constructing a dam etc.

2. Indirect Labor Cost

Indirect labor cost is the amount spent by the factory for those workers who are not directly engaged in the production process. Indirect labor cost refers to the expenses incurred in remunerating such workers who assist the direct labor to complete the manufacturing processes. It can not be identified and measured accurately on per unit of output basis. It is incurred for the benefits of a number of cost centers. It forms a part of the overhead costs. Payment made to the sweepers, watchmen, cleaners, supervisors and accounting personnel are the examples of indirect labor cost.

Concept And Meaning Of Labor

Like materials, labor is also one of the prime inputs of production system. All manufacturing concerns require the labor for carrying out their production activities. The labor consists of workers who are essential to convert materials into finished products. The workers operate machine and perform other tasks to help convert materials into final outputs.

The labor can be either direct or indirect. The labor who is directly engaged in the conversion process is called direct labor and who is not is called indirect labor. The labor, however, should be properly utilized and satisfactorily paid in order to minimize labor turnover and labor cost. Unlike materials, labor is complex to deal with. Dissatisfied and discontented labor always results in high labor costs and low quality outputs. Therefore there should be proper planning, accounting and controlling of labor.

Concept And Meaning Of Labor cost

The payment made to the labor in exchange for its service is called labor cost, which constitutes a major part of the total cost of production. Labor cost is also commonly called wages. Labor cost or wages is one of the major elements of cost. Labor cost represents the expense incurred on both direct and indirect labor. However, labor cost is more than just wage as it includes the total amount of financial benefits given by the concern to all its workers and employees for their time and effort used in producing goods and services. It is, in fact, the financial compensation provided to the workers for their physical and mental contribution for converting raw materials into finished outputs.Labor cost includes monetary and non-monetary (fringe) benefits. Monetary benefits include basic wages, dearness allowance, employer's contribution to provident find, production bonus, pension and gratuity. Fringe benefits include subsidized food, subsidized housing, subsidized education, medical facilities and holiday pay.

The labor can be either direct or indirect. The labor who is directly engaged in the conversion process is called direct labor and who is not is called indirect labor. The labor, however, should be properly utilized and satisfactorily paid in order to minimize labor turnover and labor cost. Unlike materials, labor is complex to deal with. Dissatisfied and discontented labor always results in high labor costs and low quality outputs. Therefore there should be proper planning, accounting and controlling of labor.

Concept And Meaning Of Labor cost

The payment made to the labor in exchange for its service is called labor cost, which constitutes a major part of the total cost of production. Labor cost is also commonly called wages. Labor cost or wages is one of the major elements of cost. Labor cost represents the expense incurred on both direct and indirect labor. However, labor cost is more than just wage as it includes the total amount of financial benefits given by the concern to all its workers and employees for their time and effort used in producing goods and services. It is, in fact, the financial compensation provided to the workers for their physical and mental contribution for converting raw materials into finished outputs.Labor cost includes monetary and non-monetary (fringe) benefits. Monetary benefits include basic wages, dearness allowance, employer's contribution to provident find, production bonus, pension and gratuity. Fringe benefits include subsidized food, subsidized housing, subsidized education, medical facilities and holiday pay.

Sunday, 23 May 2010

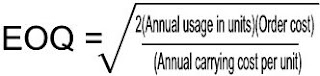

The economic order quantity can be determined in the following ways.

1. Formula Method

With the help of following formula, the economic order quantity can be calculated.

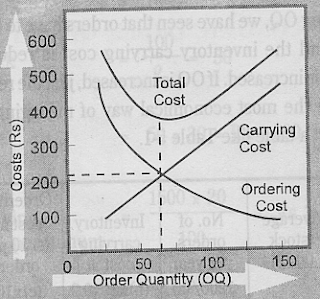

2. Graphical Method

3. Trial And Error Method

1. Formula Method

With the help of following formula, the economic order quantity can be calculated.

2. Graphical Method

Under this method, the carrying cost, ordering cost and total cost are shown on graph. It is based on the principle that the total carrying cost increases as the order size increases. However, the ordering cost decreases if the order size increases. The point at which the ordering cost and carrying cost intersects each other, total cost is minimum.

3. Trial And Error Method

If the total needs of inventory for a form are known, the firm has different alternatives to purchase its inventories. It can buy its total needs in a single order at the beginning of the year or the inventories may be purchased in small orders periodically. If the purchase are made in one order, the average inventory holdings will be relatively large whereas they will be relatively small when the acquisition of inventory is in small lots. High average inventory would involve high carrying cost and low average inventory holdings are associated with high ordering costs. According to this method, the carrying and ordering costs for different sizes of orders to purchase inventories are computed and the order size with the lowest total cost of inventory is the economic order quantity.

Thursday, 20 May 2010

Economic order quantity is also known as reorder quantity. Economic order quantity (EOQ) is a level of inventory where the total cost of holding inventory is at minimum. Economic order quantity is the level of quantity at which the cost of ordering will be equal with the storage cost of materials. In other words, the quantity of materials which is economical to be ordered at one time is known as economic order quantity. The total costs of materials consists of the ordering cost and carrying cost. While determining the economic order quantity, the ordering cost and carrying cost should be considered.

Ordering Cost

The ordering cost is the repurchase cost and is repeated in nature. Purchasing of large quantities of materials helps reduce the ordering cost. The following costs are included in the ordering cost.

* Cost of staff appointed in the purchasing, inspection and payment departments.

* Cost of stationary purchases, telephone charge, email charge, fax charge etc.

Ordering costs also includes the cost of floating tenders, the cost of making comparison among quotations, cost of paper work, cost of transpiration etc.

Carrying Cost

Carrying cost is concerned with the storage of materials. It suggests purchasing in small quantities. If small quantities of material purchased, the storing cost will below. The following costs are included in carrying costs.

* Cost of storage ( warehousing, salaries, rent etc.)

* Cost of spoilage in stores and handling

* Insurance cost of materials

* Interest on capital blocked on materials or opportunity cost

* Cost of maintaining the materials to avoid deterioration

* Cost of obsolescence due to a change in the process or product.

Tuesday, 18 May 2010

Danger level is a level of fixed usually below the minimum level. When the stock reaches danger level, an urgent action for purchase is initiated. When stock reaches the minimum level, the storekeeper must make special arrangements to get fresh materials, so that the production may not be interrupted due to the shortage of materials.

The formula for calculating the danger level is:

Danger Level = Normal consumption x Maximum re-order period for emergency purchase

The formula for calculating the danger level is:

Danger Level = Normal consumption x Maximum re-order period for emergency purchase

Illustration,

Daily Consumption = 100 to 200 units

Maximum re-order period for emergency purchase = 5 days

Danger Level = ?

Solution,

Danger Level = Normal consumption x Maximum re-order period for emergency purchase

= 150 x 5

750 units.

Average Stock level shows the average stock held by a firm. The average stock level can be calculated with the help of following formula.

Average Stock Level = Minimum Level + (1/2Re-order Quantity)

OR

Average Stock Level = (Minimum Level + Maximum Level)/2

Illustration

Average Stock Level = Minimum Level + (1/2Re-order Quantity)

OR

Average Stock Level = (Minimum Level + Maximum Level)/2

Illustration

Re-order quantity = 2000 units

Minimum Level = 500 units

Average stock level = ?

Solution,

Average stock level = Minimum level + 1/2 x Re-order quantity

= 500 + 1/2 x 2000

= 500+ 1000

= 1500 units.

Minimum Level = 500 units

Average stock level = ?

Solution,

Average stock level = Minimum level + 1/2 x Re-order quantity

= 500 + 1/2 x 2000

= 500+ 1000

= 1500 units.

Maximum level is that level of stock, which is not normally allowed to be exceeded. Beyond the maximum stock level, a blockage of capital should be exercised to check unnecessary stock. The factory should not keep materials more than the maximum stock level. It increases the carrying cost of holding unnecessary inventory level. It is the opportunity cost of holding inventory.

The maximum stock level can be calculated by using the following formula:

Maximum Level = Re-order Level + Re-order quantity - (Minimum consumption x Minimum Delivery Time)

Illustration

The maximum stock level can be calculated by using the following formula:

Maximum Level = Re-order Level + Re-order quantity - (Minimum consumption x Minimum Delivery Time)

Illustration

Re-order quantity = 1000 units

Re-order Level = 1500 units

Re-ordering period = 4 to 6 days

Daily consumption = 150 to 250 units

Maximum Level = ?

Solution,

Maximum Level = Re-order level + Re-order quantity - (Minimum consumption x Minimum Re-ordering period)

= 1500+1000(150 x 4)

= 1900 units.

Re-order Level = 1500 units

Re-ordering period = 4 to 6 days

Daily consumption = 150 to 250 units

Maximum Level = ?

Solution,

Maximum Level = Re-order level + Re-order quantity - (Minimum consumption x Minimum Re-ordering period)

= 1500+1000(150 x 4)

= 1900 units.

Minimum Stock Level

Minimum level or safety stock level is the level of inventory, below which the stock of materials should not be fall. If the stock goes below minimum level, there is a possibility that the production may be interrupted due to shortage of materials. In other words, the minimum level represents the minimum quantity of the stock that should be held at all times.

The minimum level is determined by using the following formula:

Minimum Level = Re-order level -(Normal consumption x Normal Re-order Point)

Calculation OF Minimum Level Or Safety Stock

The minimum level is determined by using the following formula:

Minimum Level = Re-order level -(Normal consumption x Normal Re-order Point)

Calculation OF Minimum Level Or Safety Stock

Illustration

Re-order Period = 8 to 12 days

Daily consumption = 400 to 600 units

Minimum Level = ?

Solution,

Minimum Level = Re-order Level - (Normal Consumption x Normal Re-order Point)

= 7200 - (500 x 10)

= 2200 units.

Working Notes:

1. Re-order Level = Maximum consumption x Maximum Re-order Point

= 600 x 12 = 7200 units

2. Normal consumption = (Maximum Consumption + Minimum Consumption)/2

= (600+400)/2 = 1000/2= 500 units

3. Normal Re-order Period = (Maximum Re-order Period + Minimum Re-order Period)/2

= (12+8)/2 = 10 days.

Re-order Period = 8 to 12 days

Daily consumption = 400 to 600 units

Minimum Level = ?

Solution,

Minimum Level = Re-order Level - (Normal Consumption x Normal Re-order Point)

= 7200 - (500 x 10)

= 2200 units.

Working Notes:

1. Re-order Level = Maximum consumption x Maximum Re-order Point

= 600 x 12 = 7200 units

2. Normal consumption = (Maximum Consumption + Minimum Consumption)/2

= (600+400)/2 = 1000/2= 500 units

3. Normal Re-order Period = (Maximum Re-order Period + Minimum Re-order Period)/2

= (12+8)/2 = 10 days.

Monday, 17 May 2010

Re-order level is a level of material at which the storekeeper should initiate the purchase requisition for fresh supplies. When the stock-in-hand comes down to the re-ordering level, it is an indication that an action should be taken for replenishment or purchase.

The re-order level is calculated as follows:

Re-order Level= Minimum Level(Safety stock) + (Average lead time x Average consumption)

ORThe re-order level is calculated as follows:

Re-order Level= Minimum Level(Safety stock) + (Average lead time x Average consumption)

Re-order Level= Maximum Consumption x Maximum Re-ordering Period

Illustration

Suppose,

Maximum consumption per day = 400 units

Minimum consumption per day = 200 units

Re-order period = 8 to 10 days

Then,

Re-order Level = Maximum consumption x Maximum re-order period

= 400 units x 10 days = 4000 units

Stock level refers to the different levels of stock which are required for an efficient and effective control of materials and to avoid over and under-stocking of materials. The purpose of materials control is to maintain the sock of raw materials as low as possible and at the same time they may be available as and when required. To avoid over and under-stocking, the storekeeper must fix the inventory level, which is also known as a demand and supply method of stock control. In a scientific system of inventory control the following levels of materials are fixed.

1. Re-order Level

2. Minimum Level Or Safety Level

3. Average stock Level

4. Danger Level

In simple average method, issue price of materials are fixed at average unit price. Simple average is an average of price without considering the quantities involved. The average price is calculated by dividing the total of the rates of the materials in the stores by the number of rates of prices.

Advantages Of Simple Average Method

Main advantages of simple average method are as follows:

1. Simple average method is very suitable when materials are received in uniform lot quantities.

2. Simple average method is very easy to operate.

3. Simple average method reduces clerical work.

Disadvantages Of Simple Average Method

Major disadvantages of simple average method are as follows:

1. If the quantity in each lot varies widely, the average price will lead to erroneous costs.

2. Costs are not fully recovered.

3. Closing stock is not valued at the current assets.

Advantages Of Simple Average Method

Main advantages of simple average method are as follows:

1. Simple average method is very suitable when materials are received in uniform lot quantities.

2. Simple average method is very easy to operate.

3. Simple average method reduces clerical work.

Disadvantages Of Simple Average Method

Major disadvantages of simple average method are as follows:

1. If the quantity in each lot varies widely, the average price will lead to erroneous costs.

2. Costs are not fully recovered.

3. Closing stock is not valued at the current assets.

Friday, 14 May 2010

Last-In-First-Out (LIFO) method follows the principle that the last items of materials purchased are issued at first. The valuation of the materials issued is made according to the latest purchase price of materials. The closing stocks of materials are valued always on the earliest prices of materials. In case of a rising price, LIFO method is suitable because material is issued at current market price.

Advantages Of LIFO Method

The main advantages of LIFO method are as follows

1. LIFO method is appropriate for matching cost and revenue.

2. LIFO method is simple to operate and easy to understand.

3. LIFO method facilitates complete recovery of material cost.

4. LIFO method is most suitable when prices are rising.

Disadvantages Of LIFO Method

The main disadvantages of LIFO method are as follows

1. Inventory valuation does not reflect the current prices and therefore are useless in the context of current conditions.

2. Due to variation of prices, comparison of cost of similar job is not possible.

3. Calculations become complicated and cumbersome when rates of receipts are highly fluctuating.

4. LIFO involves considerable clerical work.

Advantages Of LIFO Method

The main advantages of LIFO method are as follows

1. LIFO method is appropriate for matching cost and revenue.

2. LIFO method is simple to operate and easy to understand.

3. LIFO method facilitates complete recovery of material cost.

4. LIFO method is most suitable when prices are rising.

Disadvantages Of LIFO Method

The main disadvantages of LIFO method are as follows

1. Inventory valuation does not reflect the current prices and therefore are useless in the context of current conditions.

2. Due to variation of prices, comparison of cost of similar job is not possible.

3. Calculations become complicated and cumbersome when rates of receipts are highly fluctuating.

4. LIFO involves considerable clerical work.

The method in which materials are issued from the stores on a first come first serve basis is called FIFO method. In FIFO method, materials are issued strictly on a chronological order. The units of opening stocks of materials are issued first, the units from the first purchase are issued next and the closing stock is remain in stock always from the latest purchase. The value of the closing stock of materials is at the price of the latest purchase.

Advantages Of FIFO

Followings are the advantages of FIFO method.

1. FIFO method is easy to understand and operate.

2. FIFO method is useful where transactions are not voluminous and prices of materials are falling.

3. FIFO method is suitable for bulky materials with high unit prices.

4. FIFO method helps to avoid deterioration and obsolescence.

5. Value of closing stock of materials will reflect the current market price.I

Disadvantages Of FIFO

Some disadvantages of FIFO method are as follows.

1. FIFO method is improper if many lots are purchased during the period at different prices.

2. The objective of matching current costs with current revenues can not be achieved under FIFO method.

3. If the prices of materials are rising rapidly, the current production cost may be understated.

4. FIFO method overstates profit especially in inflation.

Advantages Of FIFO

Followings are the advantages of FIFO method.

1. FIFO method is easy to understand and operate.

2. FIFO method is useful where transactions are not voluminous and prices of materials are falling.

3. FIFO method is suitable for bulky materials with high unit prices.

4. FIFO method helps to avoid deterioration and obsolescence.

5. Value of closing stock of materials will reflect the current market price.I

Disadvantages Of FIFO

Some disadvantages of FIFO method are as follows.

1. FIFO method is improper if many lots are purchased during the period at different prices.

2. The objective of matching current costs with current revenues can not be achieved under FIFO method.

3. If the prices of materials are rising rapidly, the current production cost may be understated.

4. FIFO method overstates profit especially in inflation.

Thursday, 13 May 2010

There are various methods in use of pricing issues of materials from store. The selection of suitable method is significant from the viewpoint of cost absorbed and consequently on profit. Therefore, the method should be selected in the light of probable effects on profit over a period of years.

Material is purchased specially for a job. The material issued is charged to the job at its landed cost. Landed cost include the invoice price, freight, cartage and insurance charges on materials. Issue of such items can not be linked with a particular 'lot' and therefore, exact landed cost of the particular unit issued can not be identified. If the purchase price for each lot is different from that of the others, the question arises as to which purchase should be taken into consideration for pricing material issues.

Some important and mostly used methods of pricing are as follows.

1. First In First Out(FIFO) Method

2. Last In First Out(LIFO) Method

3. Simple Average Method(SAM)

Some important and mostly used methods of pricing are as follows.

1. First In First Out(FIFO) Method

2. Last In First Out(LIFO) Method

3. Simple Average Method(SAM)

Meaning of perpetual inventory system

Perpetual inventory system is also known as "Automatic Inventory System". Perpetual inventory system is a technique of controlling stock items by maintaining store record in a manner such that stock balances at any point of time are readily available. The terms 'Perpetual Inventory' refer to the system of record-keeping and a continuous physical verification of stocks, with reference to store records.

Functions Of Perpetual Inventory System

The main functions of perpetual inventory system are as follows.

1. Recording store receipts and issues to determine the stock in hand at any time, in quantity or value or both, without the need for physical counting of the stock.

2. Continuous verification of the physical stock with reference to the balance recorded in the store record is convenient for the management.

Advantages Of Perpetual Inventory System

* Perpetual inventory system provides an opportunity to verify the physical stock of materials.

* Perpetual inventory system helps in rapid stock checking which, in turn, helps in the preparation of interim accounts.

* A moral check on the store staff to maintain proper stock records.

* The investment in materials and supplies may be kept at the lowest point.

* It is not necessary to stop the production so as to carry out a complete physical stocktaking.

* Perpetual inventory system helps to avoid deterioration, obsolescence etc.

* Perpetual inventory system helps to discover or find out discrepancies and errors and remedial action can be taken quickly.

* Timely replenishment of stock is facilitated by means of recording the level specified in the bin card.

The main functions of perpetual inventory system are as follows.

1. Recording store receipts and issues to determine the stock in hand at any time, in quantity or value or both, without the need for physical counting of the stock.

2. Continuous verification of the physical stock with reference to the balance recorded in the store record is convenient for the management.

Advantages Of Perpetual Inventory System

* Perpetual inventory system provides an opportunity to verify the physical stock of materials.

* Perpetual inventory system helps in rapid stock checking which, in turn, helps in the preparation of interim accounts.

* A moral check on the store staff to maintain proper stock records.

* The investment in materials and supplies may be kept at the lowest point.

* It is not necessary to stop the production so as to carry out a complete physical stocktaking.

* Perpetual inventory system helps to avoid deterioration, obsolescence etc.

* Perpetual inventory system helps to discover or find out discrepancies and errors and remedial action can be taken quickly.

* Timely replenishment of stock is facilitated by means of recording the level specified in the bin card.

Following are the main differences between bin card and store ledger.

1.User

Bin card is maintained by the storekeeper. Store ledger is prepared by cost accounting department.

2. Nature

Bin card is a record of quantity only. Store ledger is a record of quantities and values.

3. Period

In bin card, entries are made immediately after each transaction. In store ledger, entries are made periodically.

4. Posting

Postings are made before a transaction in bin card. Posting are made after a transaction in store ledger.

5. Using Department

Bin card is kept inside the store. Store ledger is kept outside the store.

1.User

Bin card is maintained by the storekeeper. Store ledger is prepared by cost accounting department.

2. Nature

Bin card is a record of quantity only. Store ledger is a record of quantities and values.

3. Period

In bin card, entries are made immediately after each transaction. In store ledger, entries are made periodically.

4. Posting

Postings are made before a transaction in bin card. Posting are made after a transaction in store ledger.

5. Using Department

Bin card is kept inside the store. Store ledger is kept outside the store.

The following are the important store record methods that are used for keeping records of the various items of store.

1. Bin Card

Bin card is also known as a bin tag or stock card. A bin is a place, rack or cupboard where materials have been kept. Quantitative records of receipts, issues and closing balance of items of store are shown in a bin card. separate bin cards are maintained for each item and are placed in shelves or bins or are suitably hung up as it convenient. The bun gives a description, a code number of material, bin number, maximum and minimum stock level.

2. Two Bin System

In some manufacturing companies, a bin is divided into two parts: a smaller and larger one. The smaller bin stores the quantity equal to the minimum quantity and the larger part stores the remaining quantity. The quantity in the smaller part is not issued so long as the quantity is available in the larger part. New supply is ordered as soon as the larger bin is empty. Thus, the two bin system facilitates a physical review of stock by the storekeeper for the purpose of purchase requisitions.

3. Store Ledger

A store ledger is a record of stocks, both in quantity and value and is maintained by the store accounting section. Store ledger consists of the same column of a bin card, but in addition, there is an amount column, in which the values are entered. Thus this ledger provides information for the pricing of materials issued and the value of materials at any time.

1. Bin Card

Bin card is also known as a bin tag or stock card. A bin is a place, rack or cupboard where materials have been kept. Quantitative records of receipts, issues and closing balance of items of store are shown in a bin card. separate bin cards are maintained for each item and are placed in shelves or bins or are suitably hung up as it convenient. The bun gives a description, a code number of material, bin number, maximum and minimum stock level.

2. Two Bin System

In some manufacturing companies, a bin is divided into two parts: a smaller and larger one. The smaller bin stores the quantity equal to the minimum quantity and the larger part stores the remaining quantity. The quantity in the smaller part is not issued so long as the quantity is available in the larger part. New supply is ordered as soon as the larger bin is empty. Thus, the two bin system facilitates a physical review of stock by the storekeeper for the purpose of purchase requisitions.

3. Store Ledger

A store ledger is a record of stocks, both in quantity and value and is maintained by the store accounting section. Store ledger consists of the same column of a bin card, but in addition, there is an amount column, in which the values are entered. Thus this ledger provides information for the pricing of materials issued and the value of materials at any time.

Wednesday, 12 May 2010

Concept And Meaning Of Classification And Codification Of Materials

Classification and codification of materials are steps in maintaining stores in a systematic way. Materials are classified in such way that storing, issuing and identifying of materials become easy. Generally, materials are classified on the basis of their nature. Materials can also be classified on the basis of quality and utility. For example, materials may be classified as raw materials, consumable stores, components, spares and tools. Thus classifying materials on different bases such as nature, quality and utility is called classification of materials.

Classification and codification of materials are steps in maintaining stores in a systematic way. Materials are classified in such way that storing, issuing and identifying of materials become easy. Generally, materials are classified on the basis of their nature. Materials can also be classified on the basis of quality and utility. For example, materials may be classified as raw materials, consumable stores, components, spares and tools. Thus classifying materials on different bases such as nature, quality and utility is called classification of materials.

For the purpose of identification and convenience in storage and issue of materials, each item of material is given a distinct name. Such a process of giving distinct names and symbols to different items of materials is called codification of materials. Good store-keeping requires proper classification and codification of various items of stores on stock. Stores are generally classified either by their nature or by their usage. The former method of classification or classification by the nature of materials is most commonly used. Under this method of classification, the various items of stores are divided into specific groups like construction materials, belting materials, consumable stores, spare parts and so on. All the items are grouped, so that each item of stores will be conveniently codified on alphabetical, numerical or alpha-numerical basis and given a distinctive store code number.

Numerical Codification System

In numerical codification, each item is allotted a number, The numbering may be straight or in groups or blocks. This method is very suitable for those companies where the number of items are very large.

Alphabetical Codification System

In alphabetical codification, each item is denoted by a combination of the alphabets, for example, A for nut, B for screw and so on. This system is not suitable if there are large number of store items.

Alpha-numeric Codification System

In alpha-numeric codification, alphabets along with numbers are used for coding.

Decimal Codification System

The decimal codification system is more commonly used. The number of digits in the code will depend upon the extent of classification required. The greater the number of details to be covered, the greater will be the number of digits.

Advantages Of Classification And Codification Of Materials

Following are the advantages of classification and codification of materials

*Quick and easy identification of materials.

* Helps ensure a proper material control.

* Secrecy of materials.

* Saving of time in material handling.

* Eliminating the chances of wrong issue.

Numerical Codification System

In numerical codification, each item is allotted a number, The numbering may be straight or in groups or blocks. This method is very suitable for those companies where the number of items are very large.

Alphabetical Codification System

In alphabetical codification, each item is denoted by a combination of the alphabets, for example, A for nut, B for screw and so on. This system is not suitable if there are large number of store items.

Alpha-numeric Codification System

In alpha-numeric codification, alphabets along with numbers are used for coding.

Decimal Codification System

The decimal codification system is more commonly used. The number of digits in the code will depend upon the extent of classification required. The greater the number of details to be covered, the greater will be the number of digits.

Advantages Of Classification And Codification Of Materials

Following are the advantages of classification and codification of materials

*Quick and easy identification of materials.

* Helps ensure a proper material control.

* Secrecy of materials.

* Saving of time in material handling.

* Eliminating the chances of wrong issue.

Concept And Meaning of storekeeper

* Maintaining the proper record of materials relating to the receipt and issue of materials.

* Checking the physical quantity of materials and verify with a bin card.

* Preventing unauthorized entrance into the store room.

* Maintaining the stock registers, entering therein all receipts, issues and balance of materials.

* Checking and controlling losses due to evaporation, leakage, theft and so on.

* Arranging for physical verification of store items periodically.

* Keeping the store always neat, clean and tidy.

* Supplying information of materials, stock position and so on whenever needed.

A manufacturing company appoints a person for careful storing and safeguarding materials in a store who is called storekeeper. A storekeeper is a person who is the chief of stores and who is given the responsibility of store management. Storekeeper is responsible for safeguarding the materials and supplies in proper place until they are required for production activities. A storekeeper should be well-experienced, well-trained, honest and familiar with the tricks of store-keeping.

The main functions of storekeeper are as follows.* Maintaining the proper record of materials relating to the receipt and issue of materials.

* Checking the physical quantity of materials and verify with a bin card.

* Preventing unauthorized entrance into the store room.

* Maintaining the stock registers, entering therein all receipts, issues and balance of materials.

* Checking and controlling losses due to evaporation, leakage, theft and so on.

* Arranging for physical verification of store items periodically.

* Keeping the store always neat, clean and tidy.

* Supplying information of materials, stock position and so on whenever needed.

Location of stores means the place where the stores are situated. The location of stores should be carefully planned for a maximum efficiency. Store should be located near the materials receiving departments and materials user departments. The following factors are important for deciding the location of the store.

* Heavy and bulky items should be stocked very close to user department.

* The store should be located near a road or railway.

* The receiving department should also be in proximity to the store god owns

* The store should be centrally situated so as to be easily accessible.

* Similar types of materials should be stored in one place.

* Stores should be situated in safe places.

Concept And Meaning Of Central Store With Sub Stores

This is a mixed store system, a mix of centralized and decentralized stores. Under this store system, sub-stores are established in different departments according to the requirement of the company. Sub-stores are maintained at each department when the central store is at a distance from the production department. Such sub-stores are managed and controlled bu the central store itself. At the beginning of a period, the central store issues a fixed quantity of materials to the sub-stores. At the end of the period, sub-stores send a filled requisition form to the central store to maintain the stock to a predetermined level.

Advantages Of Central Stores With Sub-stores

1. Overcoming the demerits of centralized stores.

2. Offering an easier location for storing of materials.

3. Avoiding delay in issuing materials.

4. Providing services to meet the special needs of individual departments.

5. Reducing the internal transportation cost.

Disadvantages Of central stores with sub-stores

1. High cost for stationary and staffing.

2. High material handling cost.

3. More time in stock taking.

4. Extra set-up cost.

5. Complicated store control.

This is a mixed store system, a mix of centralized and decentralized stores. Under this store system, sub-stores are established in different departments according to the requirement of the company. Sub-stores are maintained at each department when the central store is at a distance from the production department. Such sub-stores are managed and controlled bu the central store itself. At the beginning of a period, the central store issues a fixed quantity of materials to the sub-stores. At the end of the period, sub-stores send a filled requisition form to the central store to maintain the stock to a predetermined level.

Advantages Of Central Stores With Sub-stores

1. Overcoming the demerits of centralized stores.

2. Offering an easier location for storing of materials.

3. Avoiding delay in issuing materials.

4. Providing services to meet the special needs of individual departments.

5. Reducing the internal transportation cost.

Disadvantages Of central stores with sub-stores

1. High cost for stationary and staffing.

2. High material handling cost.

3. More time in stock taking.

4. Extra set-up cost.

5. Complicated store control.

Tuesday, 11 May 2010

Meaning Of Decentralized Stores

{kind=link}

A decentralized store is that type of store which receives materials for and issues them to only one department and not to the whole company. The decentralized store may be in many numbers in the company, as each department has its own such store. Purchasing and handling of materials are undertaken by each and every department separately. If the volume of material activities is large, this type of store is suitable because each and every branch has their own store for facilitating smooth operations of their production activities.

Advantages Of Decentralized Stores

1. Controlling a and storing function can be accomplished easily.

2. Delay in material handling will be eliminated.

3. Minimizes the chances of loss by fire.

4. No need of internal transportation costs.

5. Specific needs of individual departments can be easily fulfilled.

6. Saving in material handling cost.

Disadvantages Of Decentralized Stores

1. Higher cost of supervision.

2. More space is required for individual departments.

3. Higher amount of investment is required.

4. More time for stock taking and taking.

5. Higher cost of staff and stationary.

6. Improved technique is less possible for controlling of materials.

Advantages Of Decentralized Stores

1. Controlling a and storing function can be accomplished easily.

2. Delay in material handling will be eliminated.

3. Minimizes the chances of loss by fire.

4. No need of internal transportation costs.

5. Specific needs of individual departments can be easily fulfilled.

6. Saving in material handling cost.

Disadvantages Of Decentralized Stores

1. Higher cost of supervision.

2. More space is required for individual departments.

3. Higher amount of investment is required.

4. More time for stock taking and taking.

5. Higher cost of staff and stationary.

6. Improved technique is less possible for controlling of materials.

Meaning of centralized stores

A centralized store is that store which receives materials for and issues them to all departments, divisions and production floors of the company. Such a store is only one in the company which receives materials for and issues to all who need them. The materials required for all the departments and branches are stored and issued by only one store.

Advantages Of Centralized Stores

The followings are the main advantages of centralized stores.

1. A better supervision of store is possible because the store is located under a single supervision.

2. A better layout of store and its control are possible.

3. Less space is occupied.

4. Investment in stock is minimized.

5. It is economical for storing materials.

6. Safety of materials is possible according to the nature of materials.

7. Trained and specialized persons can be appointed.

8. Wastage of materials can be minimized.

Disadvantages Of Centralized Store

The followings are the main disadvantages of centralized stores.

1. Delay in sending materials to the departments and branches.

2. Increase in material handling cost.

3. Greater risk of loss by fire.

4. Not suitable for a large company.

A centralized store is that store which receives materials for and issues them to all departments, divisions and production floors of the company. Such a store is only one in the company which receives materials for and issues to all who need them. The materials required for all the departments and branches are stored and issued by only one store.

Advantages Of Centralized Stores

The followings are the main advantages of centralized stores.

1. A better supervision of store is possible because the store is located under a single supervision.

2. A better layout of store and its control are possible.

3. Less space is occupied.

4. Investment in stock is minimized.

5. It is economical for storing materials.

6. Safety of materials is possible according to the nature of materials.

7. Trained and specialized persons can be appointed.

8. Wastage of materials can be minimized.

Disadvantages Of Centralized Store

The followings are the main disadvantages of centralized stores.

1. Delay in sending materials to the departments and branches.

2. Increase in material handling cost.

3. Greater risk of loss by fire.

4. Not suitable for a large company.

Monday, 3 May 2010

Concept And Meaning Of Store-Keeping

A store refers to raw materials, work-in-progress and finished goods remaining in stock. Store-keeping means the activities relating to purchasing, issuing, protecting, storing and recording of the materials. Store-keeping includes the receipts and issues of materials, their recording, movements in and out of the store and safeguarding of materials. The store is a service department headed by a store-keeper who is responsible for a proper storage, protection and issue of all kinds of materials.

Objectives Of Store-keeping

The following are the main objectives of store-keeping

* To avoid over and under-stocking of materials.

* To maintain systematic records of materials.

* To protect materials from losses and damages.

* To minimize the storage costs of materials

Types Of Stores

Generally, there are three types of stores

1. Centralized Stores

2. Decentralized Stores

3. Centralized Stores With Sub-stores

Purchasing of materials involves a number of steps, which may be different from one company to another. Generally, following steps are involved in purchasing and receiving materials.

1. Purchase Requisition

A purchase requisition is a formal request initiated by the store-keeper. The purchase requisition can also be initiated by other departments for purchase of special items not normally stocked. With the help of purchase requisition, the purchase manager comes to know the types of materials required for different departments. Generally, printed forms are used for this purpose. It is prepared in three copies. Each of the three copies is sent to the purchasing department, initiating department and accounting department respectively. Only an authorized person should sign a purchase requisition.

Purchase requisition has three purposes

* To inform purchasing department of the need to purchase materials.

* To fix the responsibility of the department making the purchase requisition.

* To use for further reference.

1. Purchase Requisition

A purchase requisition is a formal request initiated by the store-keeper. The purchase requisition can also be initiated by other departments for purchase of special items not normally stocked. With the help of purchase requisition, the purchase manager comes to know the types of materials required for different departments. Generally, printed forms are used for this purpose. It is prepared in three copies. Each of the three copies is sent to the purchasing department, initiating department and accounting department respectively. Only an authorized person should sign a purchase requisition.

Purchase requisition has three purposes

* To inform purchasing department of the need to purchase materials.

* To fix the responsibility of the department making the purchase requisition.

* To use for further reference.

2.Request For Quotations Or Tenders

After receiving a purchase requisition, the next step of purchase procedure is to find the convenient and economical sources of supply. The purchase department must maintain a list of suppliers. Selection of a particular supplier is usually made after inviting tenders or quotations from possible sources of supply. Invitations for tender in a prescribed format are sent to prospective suppliers. It contains detailed information about the availability of goods, price of materials and terms and conditions of purchasing. Tenders are received in sealed covers before the due date expires and are opened on the date fixed for the purpose.

3. Purchase Order

After completion of the above procedure, the purchase department prepares a purchase order for the supply of materials. The purchase order is a contractual agreement with the supplier for the supply of materials. Purchase order is prepared in five copies, the original copy is sent to the supplier, the second copy for receiving department, third for account department, fourth for initiating department and fifth one is retained in the purchasing department for reference.

4. Receiving And Inspecting Materials

The receiving department should perform the function of unloading and receiving of materials dispatched by the supplier. The receiving department verifies the materials with the help of a delivery note and the copy of the purchase order after receiving the delivery of goods. The supplier sends detailed information and an invoice of the materials supplied by it. It has to verify and check the quantity and physical condition of materials by making a comparison of the purchase order and the materials received.

5.Checking And Passing Bills For Payment

When the invoices are received from the supplier, they are sent to the store and accounting departments for the verification of the quality and price of materials mentioned in the invoices. After checking the required documents, the store department requests the accounting department for making the payment of the invoice to the supplier.

Saturday, 1 May 2010

Concept And Meaning Of Decentralized Purchasing

Decentralized purchasing refers to purchasing materials by all departments and branches independently to fulfill their needs. Such a purchasing occurs when departments and branches purchase separately and individually. Under decentralized purchasing, there is no one purchasing manager who has the right to purchase materials for all departments and divisions. The defects of centralized purchasing can be overcome by decentralized purchasing system. Decentralized purchasing helps to purchase the materials immediately in case of an urgent situation.

Advantages Of Decentralized Purchasing

- Materials can be purchased by each department locally as and when required.

- Materials are purchased in right quantity of right quality for each department easily.

- No heavy investment is required initially.

- Purchase orders can be placed quickly.

- The replacement of defective materials takes little time.

Disadvantages Of Decentralized Purchasing

- Organization losses the benefit of a bulk purchase.

- Specialized knowledge may be lacking in purchasing staff.

- There is a chance of over and under-purchasing of materials.

- Fewer chances of effective control of materials.

- Lack of proper co-operation and co-ordination among various departments.

Concept And Meaning Of Centralized Purchasing

Centralized purchasing refers to the purchase of materials by a single purchase department. This department is headed and managed by a purchasing manager. Under centralized purchasing, all purchases made by the purchase department to avoid duplication, overlapping and the non-uniform procurement. A company has to follow the centralized purchasing of materials for ensuring proper materials control as well as efficient store keeping. Under this system, the purchasing department purchases the required materials for all the departments and branches of the company.

Advantages Of Centralized Purchasing

- Bulk quantity of materials can be purchased at a low price with favorable purchasing terms.

- The service of an efficient , specialized and experienced purchase executive can be obtained.

- Better layout of stores is possible in centralized stores.

- Economy in recording and systematic accounting of materials.

- Transportation costs can be reduced because bulk quantity of materials purchased.

- Centralized purchasing avoids reckless purchases.

- Centralized purchasing discourages duplications of efforts.

- Centralized purchasing helps to maintain uniformity in purchasing policies.

- Centralized purchasing helps to minimize the investment on inventory.

Disadvantages Of Centralized Purchasing

- High initial investment has to be made in purchasing.

- Delay in receiving materials from the centralized store by other departments.

- Centralized purchasing is not suitable, if branches are located at different geographical locations.

- In case of an emergency, materials can not be purchased from local suppliers.

- Defective materials can not be replaced timely.

Concept And Meaning Of Purchasing

Purchasing involves acquiring materials of right quality, at the right quantity, at right time from a right source and at a reasonable price. A separate purchase department should be established to perform purchasing activities. The size of purchasing department depends upon the quantity to be purchased by the company. The purchase department determine the quality, quantity, items,price and time of purchase of materials. The function of purchase department is to purchase materials , supplies , machines and tools at the most favorable terms and conditions in a way that helps maintain the quality. It is an important function of material management and control .

Concept And Meaning Of Purchase Control

A manufacturing company is required to invest a huge amount of money in purchasing materials. It is, therefore, essential to exercise a proper material and purchase control. Purchase control refers to the purchase of materials of right quality in a right quantity at a reasonable price and at a right time. It requires a good amount of attention to the purchasing procedures of materials relating to cost, quality, volume, time, and delivery of materials. Purchase control starts with the issue of materials requisition and ends with the receipt of materials and payment of the cost of the materials.

Concept And Meaning Of Purchase Control

A manufacturing company is required to invest a huge amount of money in purchasing materials. It is, therefore, essential to exercise a proper material and purchase control. Purchase control refers to the purchase of materials of right quality in a right quantity at a reasonable price and at a right time. It requires a good amount of attention to the purchasing procedures of materials relating to cost, quality, volume, time, and delivery of materials. Purchase control starts with the issue of materials requisition and ends with the receipt of materials and payment of the cost of the materials.

Subscribe to:

Posts (Atom)